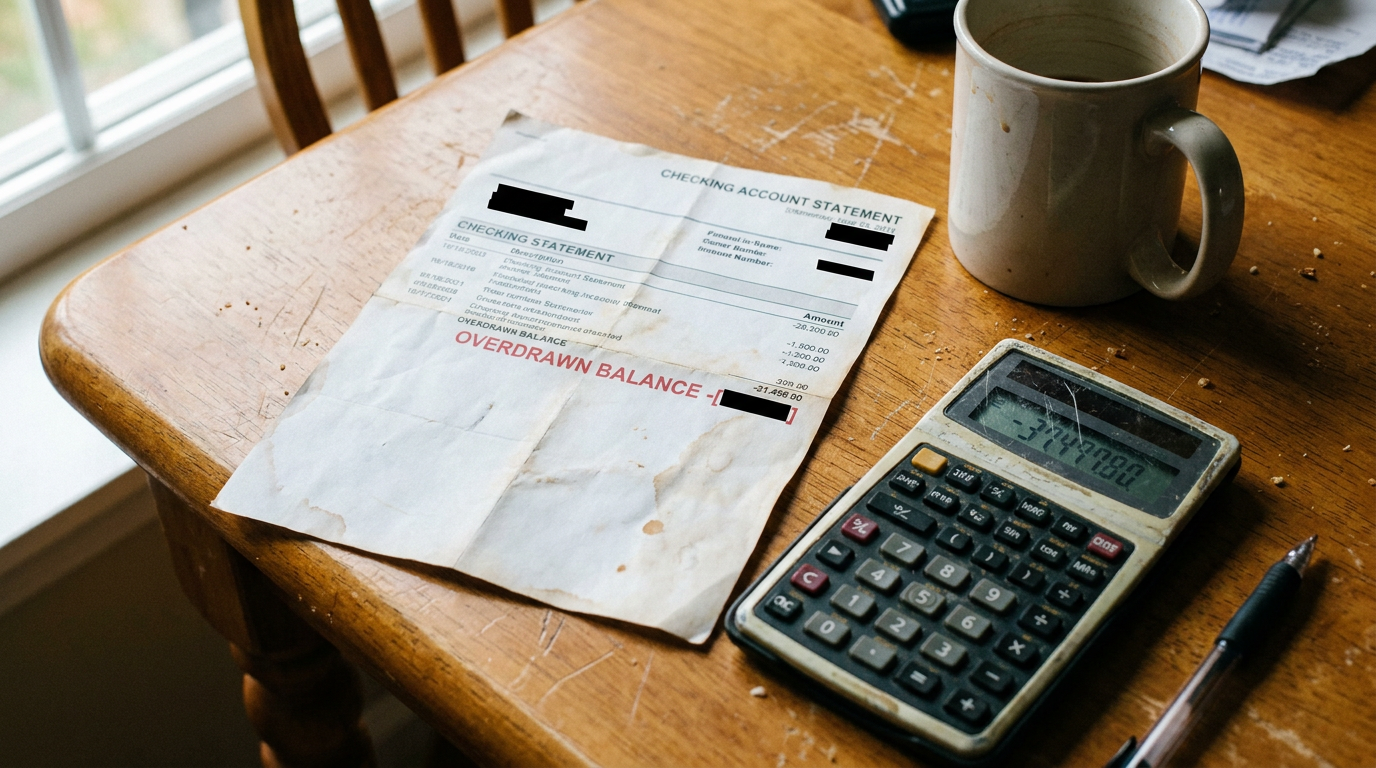

That Overdraft Line on Your Account Is Genuinely Expensive. Here's When It's Actually OK to Use It

Nearly every German checking account comes with a Dispokredit, an overdraft line you can dip into automatically, and it's genuinely useful for exactly one purpose: bridging a short-term gap, like an unexpected school expense landing a few days before payday, not financing ongoing family life on a rolling basis. The average Dispokredit interest rate has climbed past 12 percent as of May 2024, according to Stiftung Warentest's own comparison, meaningfully higher than a standard installment loan (Ratenkredit) and rising faster than the year before. Germany's consumer protection body is direct about the real risk: this becomes a genuine debt trap specifically for lower-income households that end up permanently in the negative and unable to pay the balance down, rather than using it for the brief bridging purpose it's actually designed for. If you find your family relying on the Dispokredit for recurring, longer-term shortfalls rather than occasional short gaps, a standard installment loan is consistently the option consumer advocates recommend instead, since it comes with a fixed, much lower interest rate and an actual repayment structure.

The Official Rule

Nearly every German checking account arrives with a Dispokredit already attached, an automatic overdraft line you can draw on without a separate application, and its convenience is exactly what makes it easy to reach for more often than it’s actually designed to be used.

The Dispokredit genuinely has one clear, appropriate use: bridging a short-term gap, not financing ongoing family expenses on a rolling basis. An unexpected school trip fee or a repair bill landing a few days before your next paycheck is precisely the kind of situation it’s built for. Treating it as a standing source of extra monthly budget, rather than an occasional bridge, is where the real financial cost starts to accumulate.

| Dispokredit | Ratenkredit (installment loan) | |

|---|---|---|

| Average interest rate (May 2024) | Over 12% | Meaningfully lower |

| Best suited for | Short-term bridging only | Larger or longer-term borrowing needs |

| Repayment structure | Open-ended, no fixed schedule | Fixed schedule and rate |

The actual cost of relying on it is genuinely high, and rising. According to Stiftung Warentest’s own comparison, the average Dispokredit interest rate had climbed past 12 percent as of May 2024, almost a full percentage point higher than the previous year, and meaningfully more expensive than a standard installment loan (Ratenkredit) for the same amount borrowed.

Germany’s federal consumer protection association is direct about where this becomes a genuine problem rather than a harmless convenience. vzbv’s own position paper on Dispokredit risks specifically flags lower-income households facing rising living costs as being at real risk of ending up permanently in the negative, unable to actually pay the balance down, at which point the high interest rate compounds an already difficult situation rather than the Dispokredit functioning as the brief, helpful bridge it’s meant to be.

If your family finds itself relying on the Dispokredit for recurring shortfalls rather than occasional bridging needs, the consistent recommendation from consumer advocates is switching to a standard installment loan instead. A Ratenkredit comes with a meaningfully lower, fixed interest rate and an actual structured repayment schedule, a genuinely better fit for a longer-term or larger financial need than an open-ended overdraft balance that can persist and accumulate interest indefinitely.

What Real People Say

Families describe the Dispokredit’s convenience as exactly what makes it risky, there’s no separate application or approval moment that prompts you to stop and think about the cost, the balance simply goes negative and the account keeps working normally, which can mask how expensive that convenience actually is until an interest charge shows up.

The consistent practical advice from consumer guidance is treating any Dispokredit use as a signal worth paying attention to, not alarming if it’s a genuine one-off bridge, but worth a serious budget conversation if it’s become a monthly pattern, at which point looking into a Ratenkredit or otherwise addressing the underlying shortfall becomes the more financially sound move.

Step by Step

- Use your Dispokredit for genuine, short-term bridging only, an unexpected expense before payday, not as a regular source of extra monthly budget.

- Keep track of how often you’re actually dipping into it, occasional use is very different from a recurring monthly pattern.

- Understand the real cost: average rates above 12% as of 2024, meaningfully higher than a standard installment loan.

- If you notice recurring reliance rather than occasional bridging, treat that as a signal to address the underlying budget gap directly.

- Consider a Ratenkredit for any longer-term or larger borrowing need, rather than letting an open-ended Dispokredit balance persist and accumulate interest.

Compliance Note

This page explains general guidance on Dispokredit usage and risk in Germany, current as of mid-2026. It is not financial advice. Your specific financial situation should be assessed individually, consult your bank or a Verbraucherzentrale advisor for guidance tailored to your circumstances.

FAQ & Common Pitfalls

Our account came with a Dispokredit automatically. Is it actually OK to use it occasionally?

Yes, for exactly the purpose it's designed for: bridging a genuine short-term gap, an unexpected expense that lands a few days before your next paycheck, for example. The concern isn't occasional use, it's relying on it as an ongoing way to cover regular shortfalls in your family budget, which is where the real financial risk lives.

How expensive is a Dispokredit actually, compared to other borrowing options?

Genuinely expensive. Stiftung Warentest's own comparison found the average Dispokredit interest rate had climbed past 12 percent as of May 2024, almost a full percentage point higher than the year before, and meaningfully higher than a standard installment loan (Ratenkredit). This isn't a minor difference, borrowing the same amount through a Ratenkredit instead can genuinely cost you significantly less in interest.

What's the actual risk if we end up using it more regularly than we'd like?

The risk consumer protection bodies specifically flag is ending up permanently in the negative without being able to pay the balance down, at which point the high interest rate compounds the problem rather than the Dispokredit remaining a helpful, temporary bridge. This is described as a particular risk for lower-income households facing genuinely rising living costs, where the Dispokredit shifts from occasional tool to a recurring, expensive necessity.

If we're relying on it more than we should, what's the better alternative?

A standard installment loan (Ratenkredit) is what consumer advocates consistently point to instead, it comes with a meaningfully lower, fixed interest rate and an actual structured repayment plan, rather than an open-ended, high-interest balance that can persist indefinitely. If your family's shortfall is genuinely longer-term rather than a one-off bridging need, a Ratenkredit is worth looking into rather than continuing to rely on the Dispokredit.